For many payment professionals, underwriting feels like the finish line.

A merchant is reviewed, approved, boarded, and begins processing transactions. The application is complete, the documents are verified, and the account appears compliant.

But in reality, approval is only the beginning.

The biggest compliance risks often emerge after a merchant has already been approved. Websites change. New products are added. Marketing language evolves. Shipping destinations expand. Entire business models can shift without the processor ever receiving a new application.

This creates a fundamental challenge for payment processors: how do you ensure merchants remain compliant after approval?

The answer lies in continuous merchant compliance monitoring.

The Compliance Gap Most Processors Face

Traditional underwriting provides a snapshot of a merchant at a single moment in time.

The problem is that merchant behavior is dynamic.

A wellness merchant may launch a new product category months after approval. A CBD seller might begin marketing products in a state where they are prohibited. A supplement company could introduce claims that increase regulatory exposure. A merchant that originally sold low-risk products may gradually move into higher-risk categories.

None of these changes are visible during onboarding because they happen later.

By the time a complaint, chargeback trend, regulator inquiry, or bank review identifies the issue, the exposure has already existed for weeks or months.

This is why many processors discover compliance problems only after they become portfolio problems.

What Processors Actually Monitor

Modern compliance programs focus on monitoring merchant activity continuously rather than relying solely on initial underwriting.

Areas commonly monitored include:

Website Content Changes

Merchant websites change constantly.

New landing pages, updated product descriptions, promotional campaigns, blog content, and checkout experiences can all introduce compliance concerns.

Many processors now monitor websites for changes that could create regulatory, card network, or sponsor bank exposure.

Product Catalog Updates

A merchant’s product catalog rarely stays static.

New SKUs, restricted products, prohibited ingredients, age-restricted items, or regulated categories can appear after approval.

Continuous monitoring helps identify these changes before they create larger portfolio risks.

Marketing Claims

One of the most common sources of exposure comes from marketing language.

Merchants may unintentionally publish claims that trigger regulatory scrutiny or violate network expectations.

Monitoring systems can identify changes in product descriptions, advertisements, and promotional content that may require review.

Geographic Compliance

Compliance requirements often vary by state, city, or country.

A product that is permitted in one jurisdiction may be restricted in another.

Processors increasingly monitor whether merchants are selling products into locations where those products may not be legally permitted.

Transactional Behavior

Merchant websites tell only part of the story.

Transaction patterns can also reveal emerging risks.

Sudden volume spikes, unusual ticket sizes, changing sales patterns, elevated chargebacks, or shifts in customer geography may indicate that a merchant’s risk profile has changed since approval.

Why Manual Reviews No Longer Scale

Many processors still rely on periodic manual reviews.

The challenge is scale.

Reviewing hundreds or thousands of merchants manually is time-consuming, expensive, and inconsistent. Even highly skilled compliance teams cannot continuously monitor every merchant website, product catalog, marketing campaign, and transaction stream.

As portfolios grow, the gap between merchant activity and compliance oversight grows as well.

This is why many organizations are moving toward automated monitoring systems that operate continuously across their portfolios.

The Shift Toward Real-Time Compliance

The payments industry is increasingly recognizing that compliance is not a one-time event.

It is an ongoing operational process.

Instead of waiting for complaints, chargebacks, regulatory inquiries, or annual reviews, processors are adopting systems that identify potential issues as they emerge.

This approach allows risk teams to investigate concerns earlier, engage merchants sooner, and reduce exposure before problems escalate into enforcement actions, sponsor bank findings, or network scrutiny.

The goal is not simply to detect violations.

The goal is to identify change.

Because in high-risk commerce, change is often where risk begins.

The Future of Merchant Oversight

The most effective compliance programs no longer view underwriting and monitoring as separate functions.

Underwriting establishes the baseline.

Ongoing monitoring validates that the merchant continues operating within that baseline.

As regulatory expectations increase and merchant portfolios become more complex, processors need visibility not just into how merchants looked at onboarding—but how they operate every day afterward.

Continuous merchant compliance monitoring is quickly becoming a core component of modern risk management, helping processors identify issues earlier, protect banking relationships, and maintain healthier portfolios over time.

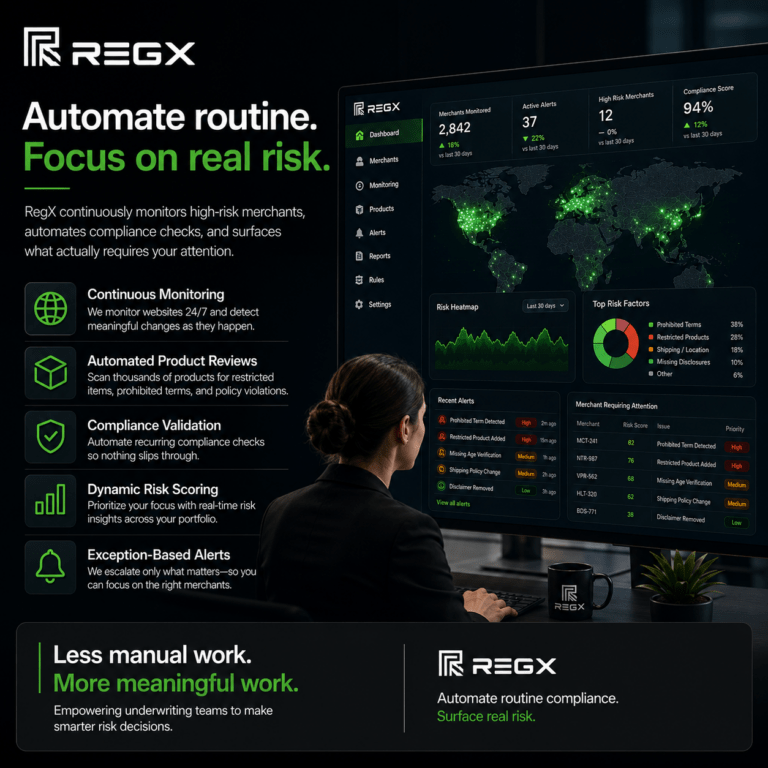

How RegX Helps

RegX provides continuous transactional compliance monitoring for payment processors, ISOs, PayFacs, and acquiring banks. By monitoring merchant activity, website changes, product offerings, and compliance indicators in real time, RegX helps organizations identify emerging risks before they become portfolio-wide problems.