Why Prevention Matters More Than Fighting Disputes Later

Most merchants think about chargebacks only after one appears.

The customer disputes the transaction. The processor sends an alert. The merchant scrambles to respond before the deadline. Evidence gets uploaded. Weeks later, a decision arrives — often after the damage is already done.

But by the time a chargeback reaches the card network, the real problem usually happened much earlier.

In high-risk commerce, chargebacks are rarely isolated events. They’re often the result of operational gaps that were already visible before the payment was ever processed.

That’s why the conversation around chargebacks is starting to shift. The smartest risk teams are no longer focused only on dispute management. They’re focused on reducing exposure before transactions ever become disputes.

And that changes everything.

The Hidden Cost of Reactive Chargeback Management

Traditional dispute workflows are reactive by design.

A merchant receives a chargeback notification, gathers evidence, submits documentation, and hopes the response is accepted. Some businesses build entire teams around representment operations.

But reactive systems have limitations:

- They start after the transaction is already considered problematic.

- They don’t address the original cause of the dispute.

- They fail to reduce long-term network exposure.

- They create operational drag for merchants, processors, and underwriting teams alike.

Worse, card networks don’t only evaluate whether disputes are won or lost. They evaluate overall dispute ratios, merchant behavior patterns, fraud signals, and operational risk trends over time.

That means even merchants with strong representment processes can still become liabilities if underlying risk signals remain unresolved.

The real goal is not simply winning disputes.

The goal is reducing the number of transactions that become disputes in the first place.

Why High-Risk Merchants Face Higher Exposure

High-risk industries operate in environments where confusion, policy changes, and regulatory inconsistencies can increase customer disputes.

A transaction may technically process correctly while still carrying elevated dispute risk because:

- Product restrictions vary by state or country.

- Buyers misunderstand what they purchased.

- Marketing language creates expectation gaps.

- Age-restricted products reach the wrong audience.

- Shipping restrictions create fulfillment issues.

- Merchants sell products banks are actively monitoring.

In many cases, the chargeback is simply the final symptom of a compliance or operational issue that existed upstream.

This is why dispute reduction cannot rely exclusively on customer service teams or post-transaction evidence packages.

The controls have to exist earlier in the transaction lifecycle.

Preventive Compliance Controls Are Becoming a Risk Tool

Preventive compliance controls are no longer just about regulation.

They are becoming part of modern chargeback mitigation strategy.

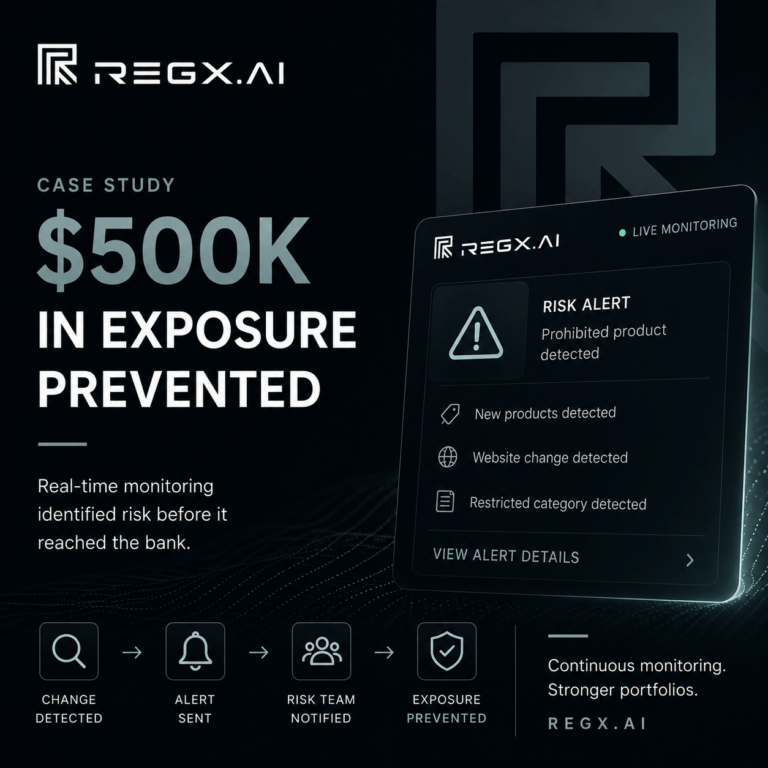

Instead of waiting for disputes to happen, processors and compliance platforms are increasingly using real-time controls that reduce risky transactions before authorization occurs.

This can include:

- Blocking transactions in restricted jurisdictions

- Detecting prohibited product combinations

- Dynamic disclaimers based on buyer location

- Age verification before checkout

- Keyword monitoring tied to underwriting policies

- Product-level restrictions tied to card brand guidance

- Research-use-only enforcement mechanisms

These controls reduce ambiguity before payment occurs.

And ambiguity is often what drives disputes.

When customers clearly understand what they are purchasing, where products can legally ship, and what restrictions apply, transaction quality improves dramatically.

The Difference Between Fraud Prevention and Compliance Prevention

Fraud tools and compliance controls are often grouped together, but they solve different problems.

Fraud systems focus on unauthorized transactions.

Compliance systems focus on authorized transactions that may still create operational, reputational, or regulatory exposure.

That distinction matters because many high-risk chargebacks are not classic fraud cases.

They are:

- “Item not as described”

- “Product unacceptable”

- “Did not understand purchase”

- “Unauthorized recurring transaction”

- “Merchant misleading”

- “Service not compliant with expectations”

Traditional fraud filters cannot solve those issues alone.

Preventive compliance controls address the root conditions that make those disputes more likely.

Why Networks Care About Early Intervention

Card networks increasingly evaluate ecosystem stability, not just individual dispute outcomes.

Processors that consistently board merchants with elevated downstream risk eventually face scrutiny themselves.

This is one reason underwriting standards are tightening across high-risk categories.

The industry is moving toward earlier detection, earlier intervention, and continuous merchant monitoring rather than static onboarding reviews alone.

The merchants that adapt fastest are usually the ones that treat compliance as operational infrastructure instead of a last-minute requirement.

Because once exposure reaches the network, options become far more limited.

The Future of Chargeback Reduction Is Preventive

For years, dispute management was treated as a back-office function.

Today, it’s becoming a transaction-layer problem.

The shift is subtle but important.

Instead of asking:

“How do we fight more chargebacks?”

Risk teams are starting to ask:

“How do we prevent avoidable disputes from ever entering the system?”

That approach reduces operational friction for merchants, lowers exposure for processors, and creates healthier long-term network relationships.

And in high-risk commerce, prevention almost always costs less than remediation.