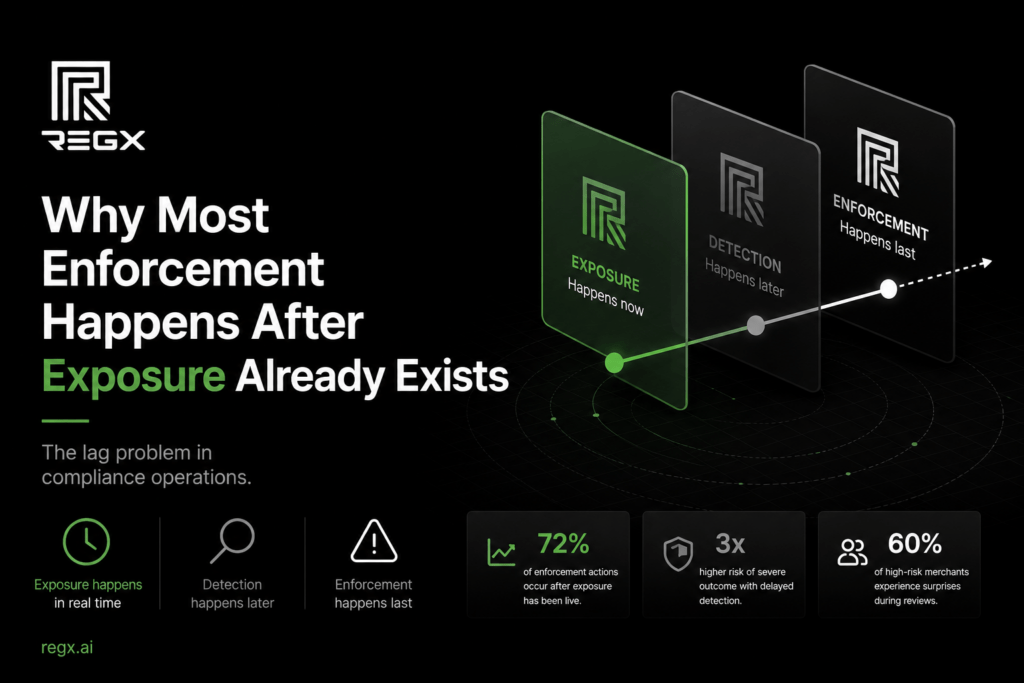

The Lag Problem in Compliance Operations

Most compliance failures don’t begin with a shutdown notice, a frozen account, or a regulator stepping in.

They begin quietly.

A product page gets updated. A state changes its rules. A disclaimer disappears during a website redesign. An affiliate starts using language that shouldn’t be there. A restricted item accidentally ships into a jurisdiction where it no longer belongs.

Nothing happens immediately.

Sales continue. Payments still process. The business assumes everything is fine.

And that’s exactly why compliance exposure becomes dangerous: enforcement usually happens long after the underlying issue already existed.

In high-risk commerce, there’s often a significant delay between when risk appears and when someone finally notices it.

That delay is one of the biggest operational weaknesses in modern compliance systems.

Compliance Problems Rarely Look Urgent at First

One of the reasons exposure grows unnoticed is because most compliance issues don’t feel dramatic in the moment.

A merchant can still have strong sales, low chargebacks, and happy customers while serious operational risk is quietly building underneath the surface.

From the outside, everything may look stable.

Meanwhile, the business may already be drifting into non-compliance through things like outdated disclosures, unsupported product language, missing documentation, or evolving state restrictions that no one internally caught in time.

This is especially common in industries where rules change quickly and businesses move even faster.

The problem isn’t always bad intent. In many cases, it’s simply operational lag.

Commerce Changes Faster Than Traditional Compliance Models

Most traditional compliance operations were built around onboarding.

A business submits paperwork. An underwriter reviews the website. Approval gets issued. The account goes live.

But modern commerce doesn’t stay still after approval.

Websites change constantly. Products rotate in and out. Marketing teams update copy. Third-party apps modify checkout behavior. New fulfillment flows appear. Laws evolve across states and cities.

The original compliance review becomes outdated almost immediately.

Yet many institutions still rely on periodic reviews instead of continuous visibility. By the time another review happens, exposure may have already existed for months.

That gap between change and detection is where most enforcement problems begin.

Enforcement Is Usually Reactive

Banks, processors, and regulators often discover issues after signals start appearing elsewhere.

A spike in disputes may trigger a deeper review. A consumer complaint may expose unsupported claims. A regulator may investigate after products have already circulated widely. A processor may reassess an account only after risk indicators begin stacking up.

In other words, enforcement tends to happen after exposure has already matured.

That creates a difficult environment for merchants. Many businesses assume silence means safety. If no warning appears, they believe operations are compliant.

But absence of enforcement does not necessarily mean absence of risk.

Sometimes it simply means nobody has looked closely yet.

Why This Creates Instability Across High-Risk Industries

Delayed enforcement doesn’t only hurt merchants.

It creates instability across the entire ecosystem.

Banks inherit preventable exposure. Payment processors face reputational and financial risk. Underwriters become more conservative toward entire categories. Legitimate businesses end up dealing with stricter scrutiny because reactive enforcement makes industries appear harder to control than they actually are.

This is part of why some high-risk sectors struggle to maintain stable banking relationships. The issue often isn’t the legality of the product itself. It’s the inability to monitor operational risk in real time.

Without continuous oversight, compliance becomes retrospective instead of preventative.

And retrospective enforcement is always more disruptive.

The Industry Is Moving Toward Continuous Compliance

The old model of “approve first, review later” is becoming harder to sustain.

Modern compliance operations are shifting toward continuous monitoring systems that evaluate risk dynamically instead of relying on static snapshots taken during onboarding.

That shift matters because today’s risk environment changes daily.

A business can become non-compliant overnight without changing ownership, processing behavior, or financial performance. Sometimes all it takes is a product update, a shipping change, or a marketing revision.

The companies adapting best to this reality are treating compliance as a live operational layer rather than a one-time approval process.

They are building systems that continuously evaluate how products are sold, marketed, fulfilled, and presented in real time.

Because in modern commerce, the biggest risk often isn’t the violation itself.

It’s the amount of time the exposure existed before anyone realized it was there.