The Problem With Static Risk Reviews in Dynamic Industries

For decades, underwriting followed a relatively simple formula.

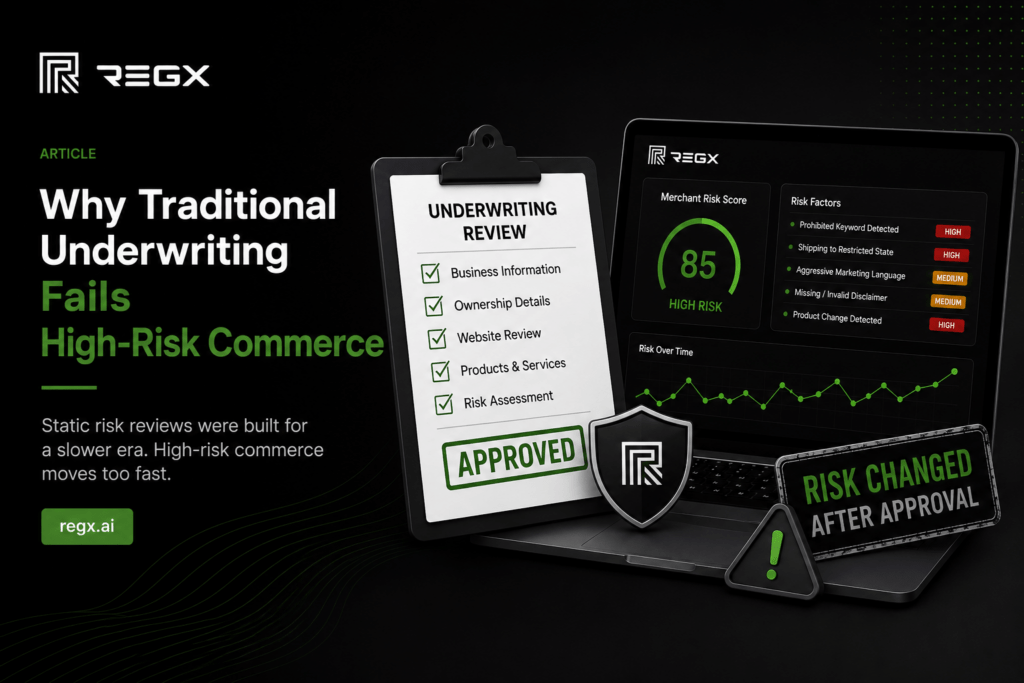

A merchant submitted documents. The processor reviewed the website, processing history, and ownership details. A risk decision was made. Then the account was either approved, declined, or monitored periodically afterward.

That model still works reasonably well for many traditional industries.

But high-risk commerce doesn’t operate like traditional commerce anymore.

Today, merchants can change their operational risk profile in days — sometimes without even realizing it themselves. Product catalogs evolve, marketing language shifts, state regulations change, and third-party traffic sources introduce entirely new compliance exposure.

Yet many underwriting systems still rely on a one-time onboarding review to evaluate businesses operating in environments that change constantly.

And that mismatch is becoming a serious problem.

The “Snapshot” Problem

Traditional underwriting is built around snapshots.

An underwriter reviews what the merchant looks like at a specific moment:

- the current website,

- current products,

- current policies,

- current marketing,

- current processing history.

But e-commerce businesses are not static.

A wellness merchant may add new products next week.

An SEO agency may rewrite product descriptions tomorrow.

An affiliate marketer may launch aggressive campaigns over the weekend.

None of those changes appear in the original onboarding package.

This creates a major blind spot between what underwriting approved and how the merchant actually operates months later.

High-Risk Industries Move Too Fast

The issue becomes even more visible in high-risk verticals because these industries evolve faster than most underwriting cycles.

Take wellness commerce as an example.

Regulations shift constantly at the state level. Card network expectations evolve. Enforcement priorities change. New product categories emerge faster than policy teams can update internal rules.

At the same time, merchants are moving quickly to stay competitive:

- launching products,

- testing landing pages,

- changing fulfillment models,

- adjusting marketing language,

- and responding to market trends in real time.

Meanwhile, many underwriting programs still rely on quarterly or annual review structures.

By the time a manual review happens, the merchant environment may already look completely different.

Financial Risk No Longer Tells the Full Story

Traditional underwriting has historically focused on financial indicators:

- chargebacks,

- fraud,

- reserves,

- processing history,

- banking exposure.

Those metrics still matter. But they often appear after operational problems already exist.

A merchant may begin making problematic claims long before chargebacks increase.

A site may start shipping into restricted states before regulators ever become involved.

A seller may quietly introduce prohibited products without immediately triggering financial alarms.

In other words, operational behavior often becomes the earliest indicator of future financial risk.

And static underwriting models are not designed to monitor operational drift in real time.

The Future Requires Continuous Visibility

This is why many processors and acquiring partners are beginning to rethink underwriting entirely.

The challenge is no longer just onboarding merchants safely.

The challenge is maintaining visibility after approval.

That means understanding how merchants evolve, how websites change, how products shift, and how compliance exposure develops over time.

Because in modern high-risk commerce, risk itself is dynamic. And static reviews can no longer fully capture dynamic businesses.