The Problem Wasn’t Underwriting

The merchant had already been approved.

The underwriting file was complete. The business had been reviewed, onboarded, and processing successfully for months. There were no unusual chargeback trends, no regulatory concerns, and no signs that the account required immediate attention.

On paper, everything looked fine.

Then the merchant changed.

Without notifying the processor, several new products were added to the website. The changes happened overnight. By the following morning, transactions were already being processed.

This is where many compliance failures begin.

Not during onboarding.

Not during underwriting.

After approval.

A Growing Blind Spot Across High-Risk Portfolios

Most processors have visibility into a merchant at the moment they are approved.

Far fewer have visibility into what happens afterward.

Merchants update websites. Product catalogs expand. Marketing language evolves. Entire categories can be added in a matter of hours.

The reality is that underwriting reviews a snapshot in time. Merchant behavior continues long after that review is complete.

In this case, the newly added products introduced a risk profile that no longer aligned with the processor’s sponsor bank requirements.

If left undetected, the merchant could have continued processing throughout the weekend, accumulating significant transaction volume before anyone noticed the change.

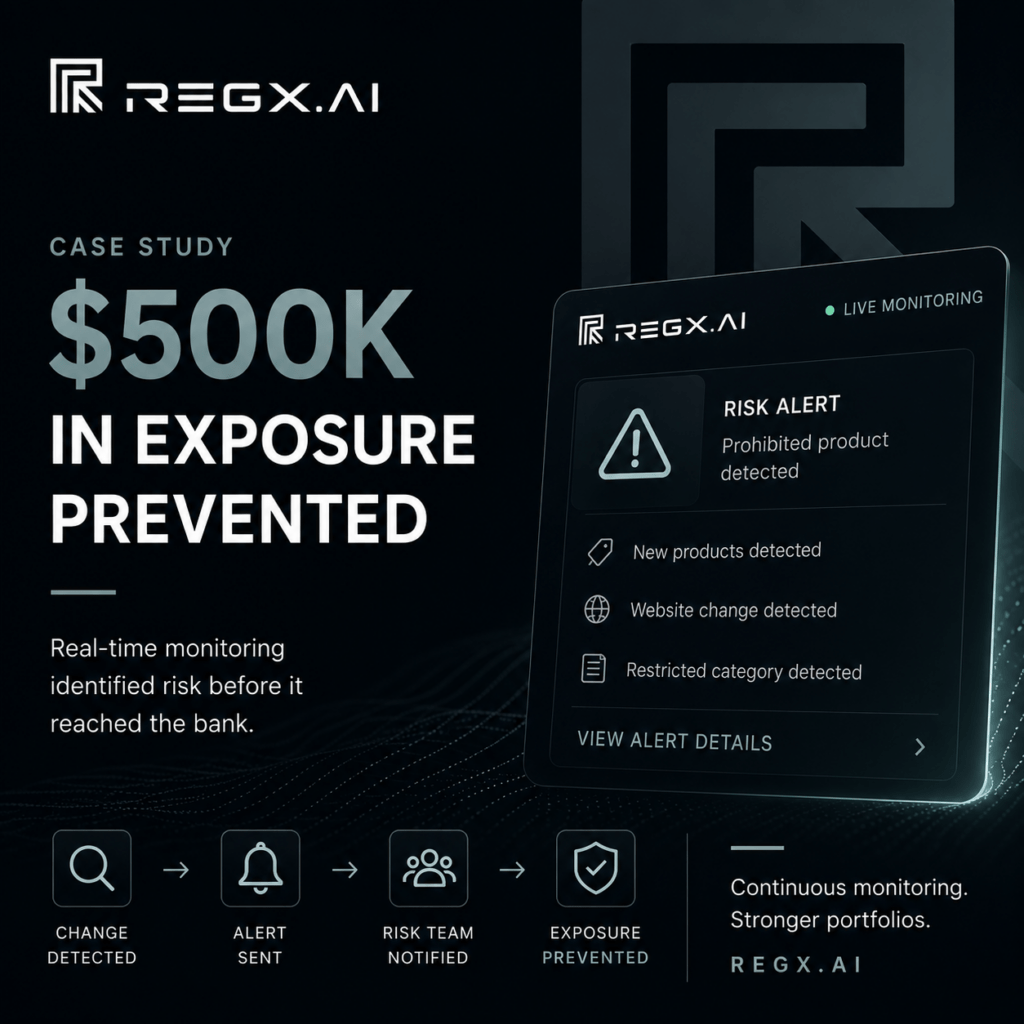

How RegX Detected the Risk

RegX continuously monitors merchant websites for changes that may create compliance, regulatory, or portfolio exposure.

Within hours of the new products being published, RegX identified multiple risk indicators:

- New products added to the catalog

- Product categories that did not exist during underwriting

- Language associated with restricted activity

- Material changes to the merchant’s approved business model

Rather than waiting for a chargeback spike, bank review, customer complaint, or network inquiry, the processor received an alert immediately.

The risk team was able to investigate the issue the same day.

The Response

After reviewing the findings, the processor contacted the merchant and confirmed that the newly launched products fell outside the parameters of the approved account.

The merchant removed the products and updated the website before significant additional volume accumulated.

No enforcement action was required.

No sponsor bank intervention occurred.

No network inquiry was triggered.

Most importantly, the issue was resolved before it had an opportunity to spread across the portfolio.

The Exposure That Never Happened

Based on the merchant’s transaction velocity and projected weekend sales volume, the processor estimated that more than $500,000 in exposure could have accumulated before the issue would have been discovered through traditional review processes.

That’s the challenge facing risk teams today.

Exposure develops quickly.

Detection often does not.

The longer the gap between a merchant change and compliance awareness, the larger the potential consequences become.

The Shift From Reactive to Proactive Compliance

Historically, compliance programs have relied on periodic reviews, chargeback monitoring, customer complaints, and enforcement actions to identify risk.

The problem is that all of those signals appear after exposure already exists.

Transactional compliance monitoring changes that model.

Instead of discovering risk after it reaches the bank, processors gain visibility into merchant changes as they occur.

That allows risk teams to address problems before they become portfolio events.

Why It Matters

For processors, ISOs, PayFacs, and acquiring banks, some of the largest compliance failures don’t come from bad underwriting decisions.

They come from merchant drift.

A merchant that was compliant yesterday may not be compliant tomorrow.

Without continuous monitoring, those changes often remain invisible until exposure has already accumulated.

The organizations best positioned to manage risk today are not the ones reacting faster.

They are the ones seeing risk sooner.

How RegX Helps

RegX provides continuous transactional compliance monitoring for processors, ISOs, PayFacs, and acquiring banks.

By monitoring merchant websites, products, categories, marketing content, and business activity in real time, RegX helps compliance teams identify emerging risk before it becomes a bank issue, a network issue, or a portfolio issue.

Because the most valuable exposure event is the one that never happens.